Portfolio personalization includes security constraints, sector constraints, custom asset allocation, social criteria restrictions, custom product selection, custom cash management, and glide paths (basically, a personalized target date fund).

Let’s take a look at these terms more closely.

Security Constraints (e.g. “Never trade IBM," “Never buy MSFT,” “Never own Ford,” “Never sell GM”):

Security constraints are the most commonly supported form of personalization and can serve many purposes:

- Ethical and legal restrictions: A lawyer whose firm represents IBM may be prohibited by their employer from trading the security. If the lawyer has access to insider information, they may be legally prohibited from trading.

- Counterbalancing employment or regional risk: If a client works for Exxon—or if they just live in Houston—they already have exposure to Exxon’s success. It may make sense not to double down on this exposure by holding Exxon in their portfolio.

- Counterbalancing outside holdings: Likewise, if a client owns shares of Exxon in another account or owns employee incentive stock options on Exxon shares, it may be prudent to avoid further exposure.

- Client personal preferences: Clients may not like a company, either because of a bad experience with the company or a general disapproval of the company’s actions, and they simply don’t want to become an owner. Conversely, they may wish to support a firm whose conduct they approve.

- Client return expectations: Clients may have negative return expectations for a security and wish to exclude it from their portfolio (or at least not buy more). Or clients may have a positive return expectation and wish to make sure they hold some minimum amount of the security in their portfolio. Most advisors discourage this sort of thing in the belief that clients are unlikely to be good at stock selection, and talking about it distracts from more important conversations about financial planning and risk control.

Sector Constraints (e.g. “Never own Energy stocks”):

The reasons for sector constraints are largely the same as those for security constraints. The most common is counterbalancing outside holdings, or counterbalancing employment or regional risk. To use the same example as above, if a client works for Exxon, lives in Houston or has outside holdings in the energy sector — they already have exposure to the success of the Energy sector, and it may make sense not to double down on this risk. Sector constraints can also be used to reflect performance beliefs.

Ethical and legal restrictions on trading an entire sector, rather than individual securities, are rarer, but we have seen it.

Custom Asset Allocations (e.g. “Reduce my Real Estate allocation to zero” “Double my Real Estate Allocation to 10%”):

Custom asset allocation is usually motivated by a desire to counterbalance outside holdings (e.g. the investor has investments in real estate not managed by their advisor). Less commonly, it is used to reflect a client’s performance beliefs.

Religious and Social Criteria Restrictions (e.g. “Apply a Catholic values screen”, “Never buy Tobacco Stocks” or “Never own securities of companies with poor toxic waste spill records”):

The motivation behind religious value and ESG constraints is straightforward: clients simply don’t wish to be an owner of a company whose business or actions they disapprove of. This decision is made independent of return expectations. Clients may in fact think that bad things will happen to bad companies. That is, they may think that these companies will perform poorly. But that isn’t the primary motivation (if it were, it wouldn't really be religious value/social criteria investing).

Social Impact Mandates (e.g. “Buy companies whose products will help the environment”):

In contrast to ESG constraints, this is a positive tilt. It’s not about avoiding the bad; it’s supporting the good.

Social impact investing is trickier than applying ESG constraints because it may be hard to create a properly diversified portfolio investing only in firms with the selected positive social impact.

Custom Security Selection (e.g. “I want to own Tesla”):

In the old brokerage model, custom security selection was, in a sense, the main form of customization—brokers talked with their clients about various stocks and jointly picked the ones the client liked best. We’ve never met an advisor who thinks this type of customization actually benefits their clients. On the contrary, advisors think it’s a distraction that reinforces a destructive view of what wealth management means and how it can help investors.

That being said, there is still a place for custom product selection. This is different than custom security selection and serves a different purpose:

Custom Product Selection (e.g. “I prefer all ETFs,” “I prefer Fidelity funds,” “I prefer a direct index for large cap US equities”):

For each asset class, clients may have a choice of how they’re going to invest. Common choices include one or more:

- ETFs

- Actively managed ETFs and mutual funds

- Actively managed proprietary basket of securities (i.e., direct ownership that bypasses the mutual fund/ETF structure)

- Actively managed basket of securities following third-party models (or an SMA managed by a third-party)

- Direct indexes

These choices come with different:

- price points (ETFs, proprietary strategies and direct indexes being the least expensive).

- levels of tax efficiency (direct indexes being the most tax efficient, then ETFs).

- minimum investments (ETFs and mutual funds having the lowest minimums).

The biggest choice in custom product selection is passive vs. active. Right or wrong, clients can hold strong beliefs in the active/passive debate, and it’s useful for firms to be able to accommodate these preferences.

The next biggest choice is commingled vehicles (like an ETF or mutual fund) vs. direct ownership of a basket of securities (e.g. a direct index). The direct ownership is both less expensive and more tax efficient, but usually requires a larger minimum investment.

Cash Management (Cash/liquidity constraints: (e.g. “Min cash = $5,000”, “Max cash = $25,000”):

Clients have different liquidity needs. Usually, this takes the form of different minimum levels of cash. It’s a minor, but very common form of customization.

Reserve Cash (e.g. “Do not invest cash if below $15,000”):

Some clients have regularly scheduled withdrawals. These clients need their cash management to be a bit forward looking. No one wants to invest cash on the 31st of a month, only to have to sell the purchased securities the next day to fund the next monthly withdrawal. The key is to set aside income up to some predetermined threshold, e.g., three months of withdrawals.

Glide Paths (e.g. “Migrate the client from an Aggressive Growth allocation to a Conservative allocation smoothly over 30 years”):

A “glide path” is like a personalized target-date fund. It’s a multi-year path for migrating a client’s asset allocation as the client ages. Typically, glide paths move clients to less aggressive asset allocations, with updates on a quarterly or annual basis.

Transition (e.g. “Trade my portfolio to be closer to its recommended asset allocation and security holdings, but don’t incur taxes on capital gains of more than $10,000/year”):

“Transitioning” is the multi-period process of migrating a client’s portfolio from its current holdings to a recommended asset allocation and security selection.

Institutional investors worry mostly about the potential market impact of large trades, and minimizing market impact is their major motivation for transitioning accounts.

In contrast, individuals are mostly motivated by tax concerns. They want to minimize gains, especially short-term gains, and spread the costs over multiple periods (either to smooth expenditures or to avoid being bumped up into a higher tax bracket). On occasion, a secondary motivation is “regret avoidance” — spreading out trades over time reduces the chance that everything is sold at a market low.

Some common tools for managing transition include:

- Tax management, especially tax budgets: (e.g. “Keep net capital gains taxes under $5,000/quarter”)

The main component of tax-sensitive transition is the same gains-deferral strategy of ordinary tax management. Phrased differently, all tax management, except for loss harvesting, is transition management — you’re managing trade-offs between taxes, drift and return expectations. Tax budgets are used to spread tax liabilities over time.

- Turnover budget: (e.g “Max 5% turnover per quarter”)

Turnover budgets are less common than tax budgets, but can be useful for comforting a client who may be uncomfortable with a single “big bang” conversion.

- Equivalence sets: (e.g. “This is my recommended holding, but the following securities are good enough and shouldn’t be sold if they’re already in the portfolio”)

While advisors and the firms they work for usually have a default recommended product for each asset class, this product may be only weakly preferred to several alternatives. If the client already owns one of these almost-as-good substitutes, there’s no real value in trading them — taxes aside, it may not even be worth the transaction costs. This logic can be addressed by setting up “equivalence sets” for every recommended security.

Tax management describes a set of practices aimed at reducing an investor’s tax bill in a way that does not interfere with the portfolio’s risk and (pre-tax) returns. The goal of tax management is to increase the investor’s expected after-tax returns – and for taxable investors, it’s after-tax returns that matter. While we are treating tax management and personalization as different things, tax management is arguably viewed simply as another type – for most investors, the most important type – of personalization.

There are at least six tools in the basic tax management toolkit:

- Short-term gains deferral:

Postponing the sale of a short-term position you might otherwise wish to sell until the position is long-term (and therefore subject to the lower long-term capital gains tax rate). - Long-term gains deferral:

Postponing the sale of long-term positions you might otherwise wish to sell. Even if you eventually do realize the gains, you will have postponed paying taxes, which you can view as an interest-free loan. If you postpone the sale until retirement, the gains may be subject to a lower tax rate. If you postpone the sale until death, you (or, more precisely, your estate) avoids the taxes completely. - Loss harvesting:

Selling a security at a loss in order to realize a loss that can be used to lower your tax bill. - Tax budget:

Keeping taxes (or just taxes from realized gains) below a predetermined threshold. The two keys to effectively implementing a tax budget are 1) taking maximum advantage of tax-loss harvesting opportunities to “buy” yourself freedom to realize more gains, and 2) optimizing how you “spend” your limited tax budget to get the biggest risk and return improvement for every tax dollar. - Tax-efficient product selection:

Purchasing securities that won’t generate a lot of taxable income because either the income is tax free or it takes the form of unrealized capital gains. Some securities are more tax efficient than others. Interest from bonds are taxed as ordinary income. The returns of some actively managed mutual funds take the form of short-term capital gains distributions. On the other hand, municipal bonds are tax free (though they also pay a lower interest rate). And index products, especially ETFs, tend to generate low capital gains distributions. - “Householding”:

Holistically managing a group of accounts (e.g., 401Ks, taxable accounts, IRAs, etc.) belonging to a single investor or household in a manner that reduces taxes, leveraging the tax-deferred accounts (e.g. the IRAs) to minimize tax on income and realized capital gains.

Tax optimization is a specialized type of tax management. All tax optimization is tax management. Not all tax management is tax optimization.

The purpose of tax management is not simply to minimize taxes. It is to minimize taxes in a way that preserves the portfolio’s desired risk/return characteristics. This involves trade-offs. For example, if you’re overweighted in IBM and your holdings of IBM have unrealized gains, you need to choose between two desirable goals: on the one, you want to sell IBM to reduce the overweight; on the other hand, you want to hold onto your IBM to avoid taxes. Any decision you make – to sell, to hold, to partially sell – involves a trade off.

Tax optimized tax management involves explicitly considering those trade-offs for every decision. In contrast, implementing simple rules like “never sell any position with short-term gains” or “loss harvest any position that is below 85% of basis” is a form of tax management, but it is not tax optimization. Tax optimization would weigh the advantages of realizing an appreciated position – even one with short-term gains – against the tax and transaction costs. With tax loss harvesting, tax optimization would balance multiple considerations: the amount of the loss, the investor’s tax rates, the quality of the substitute, even the volatility of the security (higher volatility securities have greater loss harvesting potential, so it pays to be more patient in realizing losses).

As we noted above, tax loss harvesting means selling a security not because you intrinsically want to get rid of it but in order to realize a loss that can be used to lower your tax bill.

It sounds simple enough, but the details matter:

Avoiding wash sales: In order for the loss to be realized, you must refrain for 31 days from repurchasing the security you sold (you also can’t have purchased extra holdings of the security in the previous 31 days). Otherwise, the loss is disallowed in what is called a “wash sale”.

Finding good substitutes: The need to avoid wash sales means that, for at least 31 days, you need to reinvest the proceeds of the sale in a secondary security different from the one you sold (the exact definition of “different” has never been precisely defined by the IRS). You could just hold cash, but that will cause tracking error; buying an index ETF is better; buying substitute securities in the same industry is usually best. You may be indifferent between holding the primary or the secondary, in which case the requirement that you hold a different security for 31 days is not a drawback. However, for most investors, the secondary security is at least slightly less preferred.

Covering transaction and tracking error costs: Loss harvesting, by definition, involves selling positions that, but for the tax loss, you would otherwise hold onto. This means that tax loss harvesting entails extra trading and therefore extra trading costs. This is on top of the “cost” of owning a less-desired substitute security, if only for 31 days. For tax-loss harvesting to make economic sense, the value of the tax losses has to at least equal the transaction costs, as well as the cost of being out of your preferred holdings. Otherwise, it wouldn’t be worth doing.

And this gives rise to the need for a strategy for tax loss harvesting. It’s not enough for the tax benefits of tax loss harvesting to just make up for the costs. You want to come out ahead. If you are too quick to loss harvest, most of the value of the loss harvesting will be lost to transaction costs. If you are too conservative, you’ll miss tax loss harvesting opportunities.

An optimal strategy depends on at least eight factors:

- The client’s marginal tax rates

- The ability of the client to use the losses (that is, the current or future existence of realized gains that can be offset)

- The volatility of the security

- Transaction costs

- The quality of the substitute

- {For short-term positions} The time until the position goes long term

- The time until year end

- The investor's time horizon

Tax-loss harvesting sounds like a “free lunch”, but there are three common critiques that are worth considering:

- It’s too complicated

- It’s good for a couple of years and then dries up

- It’s just delaying the inevitable

Let’s take a look at these loss harvesting objections one at a time.

Objection 1: It’s too complicated.

Loss harvesting is complicated, but only in the sense that updating spreadsheets is complicated — hard to do by hand, easy to do with computers. Sophisticated loss harvesting can be completely automated — no fuss, no muss.

Objection 2: It’s good for a couple of years and then dries up.

The concern here is that you eventually run out of loss harvesting opportunities. You eventually get “lock in” — every position at a loss has been harvested and all that is left is positions with low basis. This objection is valid up to a point. If you were to buy a portfolio and leave it alone except for loss harvesting, you would typically exhaust all loss harvesting opportunities within a few years.

But very few portfolios take the form of “invest all at once and that’s it.” Stuff happens — there are new investments, rebalancing to correct for drift, tactical asset allocation shifts, new security recommendations. Each of these will result in the purchase of new positions, creating new loss harvesting opportunities. More importantly, every one of these events creates an opportunity to reduce taxes through gains deferral. It’s not tax loss harvesting, but it’s very valuable.

Objection 3: It doesn’t cut taxes, just delays them.

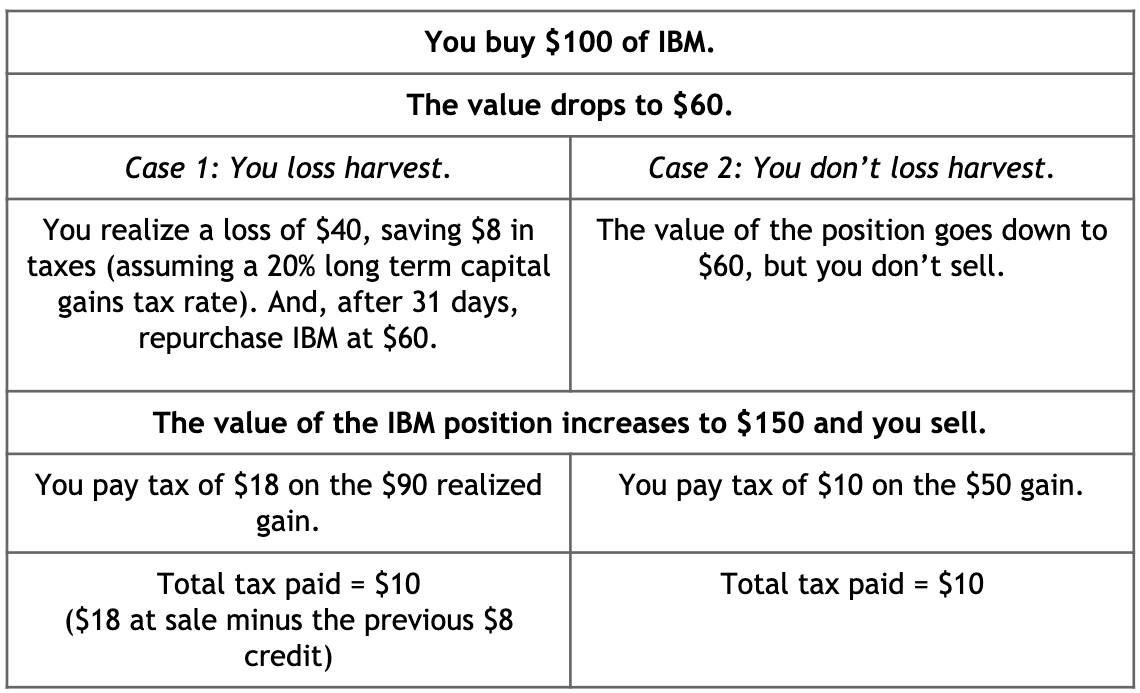

Some forms of loss harvesting don’t eliminate taxes, just delay them. Whenever you realize a loss, you’re effectively “resetting” your basis to a lower number. It’s great that you got a loss, but if and when you eventually liquidate your portfolio, you’ll pay more taxes than you would have if you had never loss harvested in the first place. We can illustrate this with an example:

So it appears that loss harvesting was all for naught, since you ended up paying $10 in taxes in both cases. But even in the case described above, you win because you ended up with an interest-free loan. You save $8 today; you pay $8 later. This is non-trivial. At a discount rate of 5%, delaying tax payment for 10 years means you’re effectively reducing your taxes by 40%. This type of tax management is called tax deferral. As the preceding “effective 40% cut” example shows, it can be quite valuable — and the longer you can defer the tax payments, the more valuable it is.

But tax deferral is just the beginning. Often, you can do better — you can defer gains and also cut the amount you actually pay. This can happen in three ways:

- You realize the loss when it is short-term but realize the gain when it is long-term. If you can realize a short-term loss to offset short-term gains but sell only when the position is long term, you save yourself the difference between short- and long-term tax rates (roughly ½). This is a double win — you’re both cutting the total tax bill AND deferring it (which gives you the interest-free loan we talked about earlier).

- You realize the loss when you’re in a higher tax bracket, but realize the gain when you’re in a lower tax bracket. Many investors don’t start drawing down their investments until retirement, when they’re in a lower tax bracket. So, as with the “realize short-term losses but long-term gains” example above, not only do they get an interest-free loan, the gains they realize are taxed at a lower rate. Again, it’s a double win.

Bottom line, the critics are wrong. Tax loss harvesting is valuable. However, in one sense, the critics are right. Loss harvesting is not the most valuable aspect of tax management. That title belongs to gains deferral. Unlike loss harvesting, where opportunities can become scarcer over time, gains deferral opportunities increase over time. The more a portfolio has embedded gains, the more important it is to be careful about what you sell. Gains deferral is important when you rebalance to correct for drift, it’s important when you implement tactical asset allocations. And it’s important when you withdraw funds from your account.

As we noted before, gains deferral is the act of holding a position that, if not for tax considerations, you would otherwise sell. There are two types of gains deferral:

- Short Term Gains Deferral: You delay selling a short-term position until it’s long term. Roughly speaking, this cuts your tax bill in half.

- Long Term Gains Deferral: You delay selling a long-term position, maybe for just a while, maybe indefinitely. If you sell eventually, you’re still getting value, in the form of a delayed (deferred) tax bill. It’s the equivalent of an interest-free loan. And if you never sell, either because you hold the position until death, or you donate the position to charity, you avoid capital gains taxes entirely.

Gains deferral sounds simple. After all, how hard is it to not sell something? But there’s more going on than just refraining from a sale. The challenge of gains deferral is to avoid selling appreciated positions while still ending up with the portfolio you want. The downside of holding onto a position for tax reasons is that you’re left owning more of the position than you want. And that means you're exposed to a particular stock’s performance more than you want to be. The key to competent gains deferral is keeping this risk under control.

How? First, actively “counterbalance” overweighted positions by underweighting securities that are most correlated with the security that is overweighted. If you’re overweighted in Exxon, underweight Chevron. The idea is to keep core “characteristics” (e.g. beta, capitalization, P/E, sector, industry, momentum, etc.) of the portfolio unchanged.

Second, don’t overdo it in the first place. If an appreciated security constitutes the majority of a portfolio, a deferral of all gains would be a case of the proverbial tax tail wagging the investment dog. How much is too much? It depends on 1) how volatile the security is, 2) your return expectations for the security, relative to alternatives, and 3) how well you can effectively undo the overweight risk through counterbalancing.

So, let’s put it all together. Well executed gains deferral means prudently holding onto overweighted positions with unrealized gains, and then minimizing the risk and return impact by carefully counterbalancing. It is an optimization problem. And, unlike loss harvesting, your work isn’t done in 30 days. You have to keep monitoring the overweighted positions and evaluating how to counterbalance the overweight for as long as you own the security.

And that’s why gains deferral is hard. Done well, it requires sophisticated optimization analytics. It is exceedingly difficult to do well manually. And it’s an open-ended commitment — maybe even a lifelong commitment if you hold overweighted positions until death.

Folks sometimes treat “tax management” and “loss harvesting” as synonyms. They’re not. Loss harvesting is an important component of tax management. But as stated previously, gains deferral is even more important. For many folks, this is a bit shocking, like learning that Sherlock Holmes has a smarter older brother (Mycroft Holmes). Loss harvesting gets the attention; gains deferral does most of the work. We can put numbers on this. We generate an “Estimated Taxes Saved or Deferred Report” for every account managed on our system, which includes taxes saved from both loss harvesting and gains deferral. It’s not a contest. For most portfolios, gains deferral is the more important source of tax savings — by more than 3 to 1 over the long term.

One of the criticisms of loss harvesting is that, on average, markets and investment portfolios go up in value, so, eventually, you have no more loss harvesting opportunities. We’ve explained why this isn’t quite true. (There’s always stuff happening, like rebalancing and cash flows, that can create new loss harvesting opportunities.) But it’s not completely false either. In a portfolio that is properly managed for taxes, you will get lots of appreciated securities. That’s bad for loss harvesting, but good for gains deferral. After a few years, gains deferral becomes the dominant tax management strategy. Unlike loss harvesting, where opportunities can become scarcer over time, gains deferral opportunities increase over time.

Given gains deferral’s status as the core of efficient tax management, why don’t we hear more about it?

One reason seems clear: implementing gains deferral manually requires a level of attention and care that is only economical for high net worth — or perhaps ultra high net worth portfolios. The good news is that modern automation tools are changing this. Sophisticated gains deferral, like sophisticated loss harvesting, can now be implemented inexpensively and at scale.

But there may be another reason why gains deferral doesn’t get the attention it deserves: Clients may value it less. It appears to be doing nothing. What client wants to pay their advisor for doing nothing? This applies double for legacy holdings — positions that the client transferred in to be managed by the advisor. Why should the client pay an advisor for holding a security that the client bought? The reasoning isn’t sound. Risk-managed gains deferral is really valuable. And hard. But it may not be highly valued by clients.

There are basically two different ways to use tax-deferred accounts in a household to lower taxes:

- Lower taxes on capital gains by using tax-deferred accounts as “tax free household-level rebalancing centers. That is, preferentially implement household-level asset-class rebalancing in tax deferred accounts

- Lower taxes on income by purchasing the least tax efficient securities (e.g., bonds, hedge funds) in tax-deferred accounts.

Note that there can be a tension between these two tax management techniques: concentrating tax-inefficient securities in tax-deferred accounts may make them less useful as tax-free tools for implementing asset-class rebalancing.

In 2022, the clients of Smartleaf users saved or deferred an average 3.07% in taxes. This is more than most advisors charge in fees. This is not an anomaly. In a recent case study, we found that 68% of accounts had, since account inception, cumulatively saved or deferred more in taxes than had been paid in fees. The figure rises to 90% on a dollar-weighted basis. Learn more in the full case study here.

No. Portfolio personalization and tax management can be automated. There need be no trade off between personalization, tax management and scale.

Yes. Common wisdom holds that centralized portfolio rebalancing is great for efficiency but terrible for personalization and tax optimization.

Common wisdom is wrong.

Relative to the alternative of having investor-facing advisors rebalance portfolios (so-called “rep as PM”), centralization does support greater efficiency. But it also supports greater personalization and superior tax management. The fact that centralization leads to greater efficiency is not surprising — the search for greater efficiency is why most centralized rebalancing groups were created in the first place. To that end, they strive to standardize and automate rebalancing to the greatest extent possible. This greater use of automation is key to the efficiency of centralized groups.

However, this same automation is also the key to enabling centralized groups to improve personalization and tax management. Because if implementing personalization requests and tax optimization are automated, you can reduce the incremental cost of managing a personalized and tax-optimized portfolio to zero. And, as with anything you make free, folks consume more of it. It becomes economically viable for firms to offer every account high levels of personalization and tax optimization. After all, it’s free, so why not make it universal?

This zero-cost personalization and tax optimization clearly makes it possible to increase the level of personalization and tax management offered to smaller accounts that previously got little or no customization. Less obviously, automation can also increase the personalization and tax optimization of larger accounts, even ultra high net worth accounts. This is because there are some types of personalization and tax management that require advanced technology that is impractical for most advisors to use. Which means that scalable, centralized rebalancing programs can increase the level of personalization and tax management provided to all clients, including UHNW accounts. Even accounts that are “custom-tailored”, accounts that are so customized that they would seem impervious to automated management, and accounts that don’t even follow a “model”.

In the past, moving towards more centralized rebalancing really did mean giving up personalization and tax management. No more. The good news is you don't have to choose between personalization and tax optimization on the one hand and efficiency or scale on the other. You (and your clients) can have both.